Homes in Denver Metro Area Surpass $410,000 Median Sales Price

Across all of Colorado, there are 30 percent fewer homes for sale across state than one year ago. Active and new listings rise but strong sales, low inventory continue to shape seller’s market.

Key findings from the June 2017 research report include:

- Peak summer housing market sees median sales prices for single family homes in the metro region, as well as statewide, increase to new record highs.

- Median sales price for single family homes in the Denver metro region rose to $411,000 while statewide that number hit $370,000.

- Despite active listings increasing 13 percent statewide and new listings rising 7 percent in the metro region and statewide, the inventory of active listings remains 30 percent lower than one year ago.

- Median sales price for a condo/townhome in Colorado rose to $275,000 11 percent higher than a year ago. Similarly, in the Denver metro region, that number hit $277,000, a 12 percent increase over a year prior.

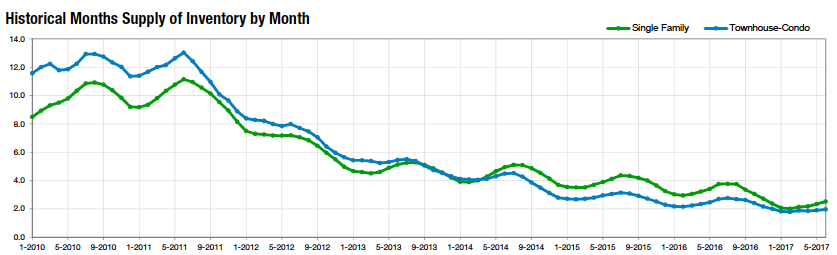

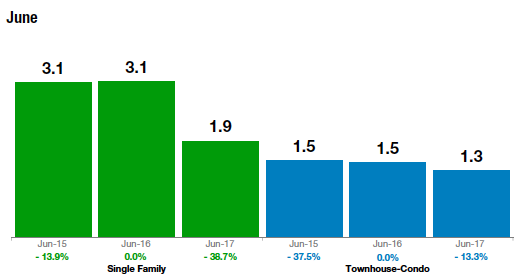

- Overall, a continued lack of inventory continues to play a major factor in the market with just 2.4 months supply of inventory across the state and 1.8 months in the Denver Metro area. Overall, inventory is down more than 31 percent across the state and more than 33 percent in the Denver metro area.

See our Regional and Statewide Statistics to see statewide or reports by county.

ENGLEWOOD, Colo. – July 13, 2017 – With the summer buying and selling season in full swing during the month of June, Colorado homebuyers and sellers watched median sales prices rise once again to new record levels, according to the June statewide housing report from the Colorado Association of REALTORS® (CAR).

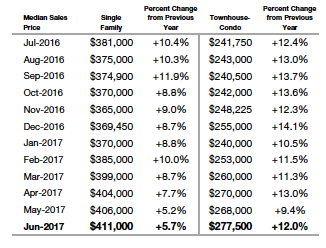

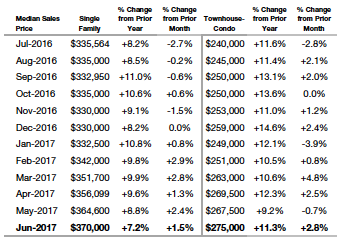

The metro region saw its median sales price reach $411,000 for single-family homes, up nearly 6 percent from a year ago, and $277,500, a 12 percent increase over a year earlier, for Denver-metro area condominium/townhomes. Statewide, the median sales price hit $370,000 for single-family homes, a more than 7 percent increase over June 2016. Statewide, the amount hit $275,000 for condominium/townhomes, an 11 percent increase year-over-year.

Despite 7 percent increases in new listings both in the metro region and statewide, and a 13 percent increase in inventory of active listings in the state from May to June 2016, a continuation of record low summertime inventory and strong buyer demand kept the state and metro region housing markets on an anticipated course in the ongoing seller’s market.

Here are a few quotes about the most recent housing market conditions from Colorado Association of REALTOR® research spokespersons representing regional markets:

“The Boulder/Broomfield housing market remains strong with an increase in prices of both attached dwellings and single-family homes already at approximately 12 percent this year. We are experiencing a typical, seasonal summer slow down with a handful of price reductions and some homes staying on the market longer. The more affordable homes are selling in under 30 days but the higher-end homes are staying on the market much longer. I predict that the majority of our appreciation has already happened and that we will cruise along to end of year with very little change. Homes priced well are moving, but those priced even a little too high are having to adjust to meet the new summer market,” said Boulder-area REALTOR® Kelly Moye.

“As the median sales price for a single-family Denver home edges ever closer to doubling in the last five years, the annual mid-season slowdown appears to be coming a little early this year. Homes priced in the affordable category continue their red-hot demand while homes above the median price of $440,000 have started to recognize nominal price decreases – especially on the higher end. As the Percent of List Price Received remains steady at 100.9 percent, even the above-average category is recognizing a strong market activity. We can expect the remainder of summer to stabilize going into the ‘back to school’ mindset within suburban areas while urban dwellings under the median mark show no signs of cooling,” said Denver-area REALTOR® Matthew Leprino.

“The median sales price for a single-family home in Jefferson county is still right around $430,000. However, the homes that are priced above $450,000 are sitting on the market just a bit longer. We still need more condo inventory with FHA financing available. While June seemed to have slowed a touch on the buy side, July seems to be revving up again. Overall, inventory remains low,” said Golden-area REALTOR® Barb Ecker.

“June was a hot townhome-condo market in Arvada. Days on market dropped almost 50 percent (46.2 percent) from the previous June. The median price of a townhome-condo increased 8.1 percent to $253,950 compared to the same month a year ago. Sellers continued to receive slightly over the list price, selling at 102 percent, the same as a year ago. As we are seeing consistently throughout the state, inventory continues to be low and that held true in the Arvada market, with active listings down 10 percent. An encouraging fact for buyers is that, if they were able to locate and successfully contract for a townhome-condo in June in Arvada they slide in slightly under the average sales price compared to the entire metro Denver market, said Arvada-area REALTOR® Karen Levine.

“Prices are stabilizing and we are seeing homes that are overpriced and sitting on the market, having price reductions. In Brighton and along the I-76 corridor, the month of June brought fewer buyers to the market. By month end the number of new listings had picked up and the buyers have come back to the market,” said Brighton-area REALTOR® Jody Malone.

“Similar to many other areas of the state, Grand Junction continues to have far more prospective buyers than inventory available. We are actually seeing some incoming buyers to our market that were not able to find homes in the Denver area but have the ability to work virtually and are buying here. Delta has been experiencing a similar boost of activity as potential Grand Junction buyers move into the Delta market. We have basically one-third of the number of homes on the market compared to last year,” said Grand Junction-area REALTOR® Ann Hayes.

“The Fort Collins Area is seeing a rise in the number of single family listings, up just over 5 percent year-to-date over last year, but sales have remained steady. With attached dwellings, listings are up nearly 19 percent year to date over last year, and sales are up over 27 percent year-to-date. Demand for homes above the upper $400s seems to have slowed significantly in the last three weeks, which may be due to the Fourth of July holiday. It may seem that the market is moving more towards stable, which would be a good thing for Buyers in Northern Colorado,” said Fort Collins-area REALTOR® Sean Dougherty.

“In the Roaring Fork and Colorado River Valleys, the lack of inventory continues to drive the market. However, prices are stabilizing and homes that are overpriced for their location or condition are starting to increase their days on market. The market in the lower valley from New Castle to Parachute seems to be more robust than that of the upper valley from Glenwood to Carbondale, where prices have increased exponentially this year over last year,” said Glenwood Springs-area REALTOR® Erin Bassett.

“The Colorado Springs-area single family/patio homes housing market had record setting sales in June 2017 with about 20 percent less active listings compared with June 2016. There was a welcome modest increase in sales of properties priced over $600,000. However, the strongest demand remained for homes priced under $300,000. Last month, 967 single family/patio homes priced under $300,000 sold while the inventory in this price range at the beginning of the month was only 551. This results in multiple, over list price offers and leads to appraisal challenges since appraisals, by their nature, are backward-looking. When markets move faster than normal, appraisal values lag market prices,” said Colorado Springs REALTOR® Jay Gupta.

“The Pueblo market remains strong with listings up 4.1 percent year-to-date. However, we remain way short of what we need in this market as we saw sold listings go up 11.6 percent year-to-date. The median sale price jumped 8.9 percent while the average sale price was up 5.5 percent as multiple offers on properties continue to drive prices up. The average number of days a for sale home stayed on the market dipped to 89. While new construction is up, it also falls well short of what is needed,” said Pueblo-West REALTOR® David Anderson.

Metro Region Median Sales Price 2017

Statewide Median Sales Price 2017

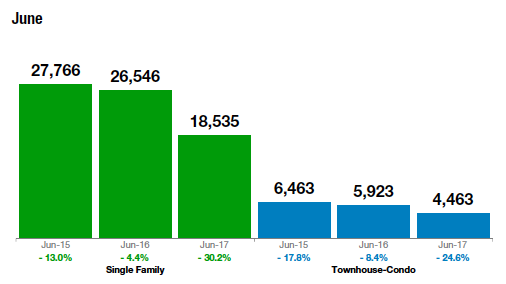

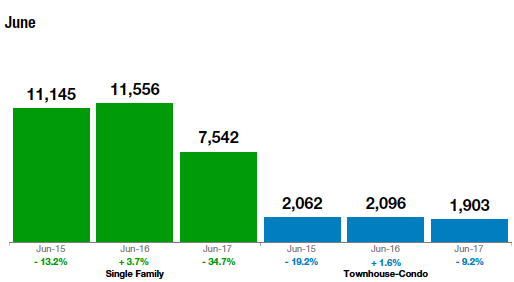

With new listings increasing nicely both in the metro region and statewide (7 percent), and active listings up 13 percent statewide and 16 percent in the metro region, there are still far fewer active listings (-28 percent) than a year ago across the state and in the Denver metro region (-31 percent).

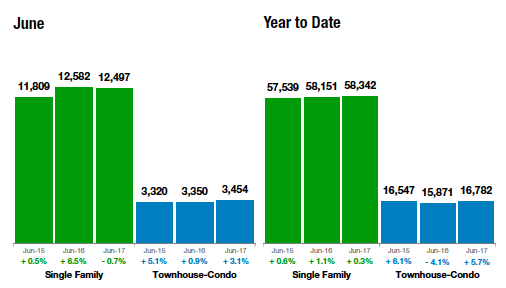

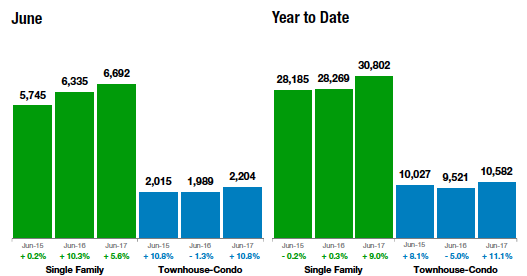

Statewide New Listings

Metro Region New Listings

Statewide Active Listings

Metro Region Active Listings

The month’s supply of housing inventory remains very low across the state at approximately 2.5 months, down more than 30 percent from a year ago. In the metro region, the supply of inventory remains below 2 months (down 39 percent from a year earlier), and as little as 1.3 months for condominium/townhomes. Balanced markets range from a 4-7 month supply.

Statewide

Denver Metro Region – Months Supply of Inventory

Also continuing its course during the month of June, the average days a for-sale home stayed on the market continued to drop. Statewide, the report shows a 42-day average for single family homes, while townhome/condo units averaged just 34 days on the market. In the Denver metro region, those numbers drop to 22 for single family homes and just 17 days from the time a townhome/condo goes on the market through closing.

The Colorado Association of REALTORS® Monthly Market Statistical Reports are prepared by Showing Time, a leading showing software and market stats service provider to the residential real estate industry, and are based upon data provided by Multiple Listing Services (MLS) in Colorado. The June 2017 reports represent all MLS-listed residential real estate transactions in the state. The metrics do not include “For Sale by Owner” transactions or all new construction.

The complete reports cited in this press release, as well as county reports are available online at: https://coloradorealtors.com/market-trends/

###

CAR/SHOWING TIME RESEARCH METHODOLOGY

The Colorado Association of REALTORS® (CAR) Monthly Market Statistical Reports are prepared by Showing Time, a Minneapolis-based real estate technology company, and are based on data provided by Multiple Listing Services (MLS) in Colorado. These reports represent all MLS-listed residential real estate transactions in the state. The metrics do not include “For Sale by Owner” transactions or all new construction. Showing Time uses its extensive resources and experience to scrub and validate the data before producing these reports.

The benefits of using MLS data (rather than Assessor Data or other sources) are:

Accuracy and Timeliness – MLS data are managed and monitored carefully.

Richness – MLS data can be segmented

Comprehensiveness – No sampling is involved; all transactions are included.

Oversight and Governance – MLS providers are accountable for the integrity of their systems. Trends and changes are reliable due to the large number of records used in each report.

Late entries and status changes are accounted for as the historic record is updated each quarter.

KEY METRICS GLOSSARY

New Listings –This is a measure of how much new supply is coming onto the market from sellers. For example, Q3 New Listings are those listings with a system list date from July 1 through September 30.

Pending/Under Contract – This is the most real-time measure possible for homebuyer activity, as it measures signed contracts on sales rather than the actual closed sale. As such, it is called a “leading indicator” of buyer demand.

Sold Listings – This measures how many home sales were actually closed to completion during the report period.

Median Sales Price – This is a basic measurement of home values in a market area and basically states that 50 percent of the homes sold were either higher or lower than the Median Sales Price.

Average Sales Price – This is another basic measurement of home values in a market.

Percent of List Price Received – The mathematical calculation of the percent difference from the list price and the sold price for those listings sold in the reported period.

Days on Market – A way to measure how long it is taking homes to sell.

Affordability – Uses median sales price, prevailing interest rates and average income to measure local housing affordability. A higher number is usually interpreted as greater housing affordability.

The Colorado Association of REALTORS® is the state’s largest real estate trade association representing more than 24,000 members statewide. The association supports private property rights, equal housing opportunities and is the “Voice of Real Estate” in Colorado. For more information, visit https://coloradorealtors.com.